Financial institutions must adhere to stringent regulatory requirements to combat money laundering, terrorism financing, and other financial crimes, as outlined by the Bank Secrecy Act, the Financial Industry Regulatory Authority (FINRA), and the Financial Crimes Enforcement Network (FinCEN). The use of Know Your Customer (KYC) checks allows organizations to obtain regulatory compliance within their sector and jurisdiction. However, KYC checks also enable businesses to strengthen their customer onboarding processes, in which they can analyze customer risk and carry out appropriate due diligence measures and KYC procedures. A risk-based approach ensures that enhanced due diligence can then be carried out only when necessary, further supporting efficiency in customer onboarding.

This strategic approach to KYC not only helps prevent financial crimes but also fosters stronger, more transparent relationships between institutions and their clients. By focusing resources where they are most needed, financial institutions can maintain compliance, mitigate risk, and improve operational efficiency, all while contributing to the broader goal of safeguarding the global financial ecosystem from illicit activities.

Scalable Onboarding with KYC Checks

Many businesses still lack automated KYC processes, so securely and effectively onboarding new customers can slow down growth and constrain operations. As businesses scale, they must implement KYC solutions that allow them to do so easily.

“Last year, the fallout of Silicon Valley Bank and Signature Bank underscored the importance of onboarding experiences. The aftermath saw a seismic shift in deposit patterns as larger banks found themselves grappling with an unexpected influx of business, overwhelming their operational capacities. One way for banks and FIs to address these challenges is through digital onboarding.”

Onboarding processes must be able to support a fast influx of new customers while still ensuring every customer’s identity is verified in accordance with KYC regulations to avoid money laundering and other types of financial crime.

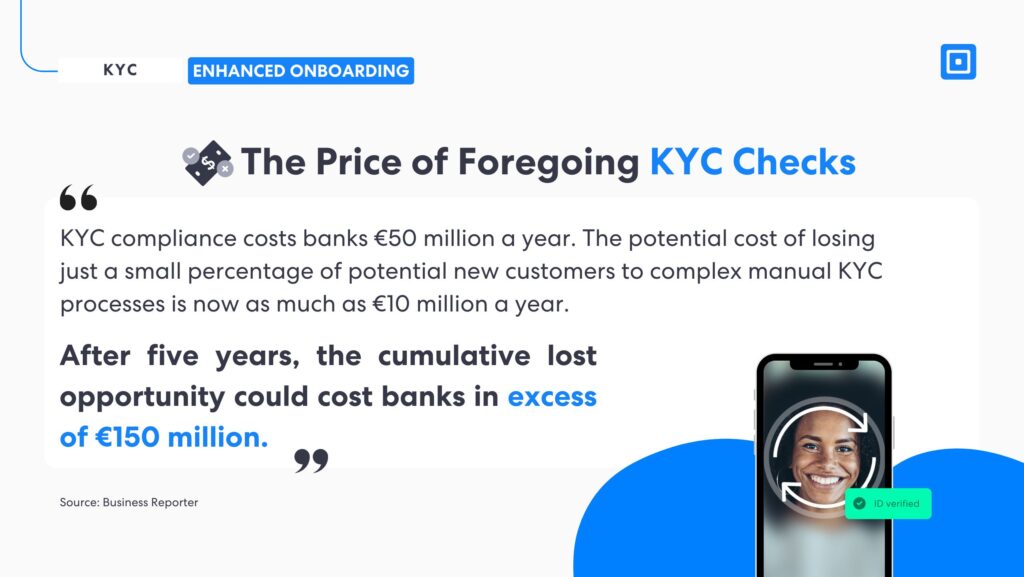

An article from the Business Reporter effectively quantified what losses can look like when onboarding processes are unable to handle large amounts of KYC checks, highlighting the risks businesses take when not adequately investing in KYC verification. “According to research conducted by Mitek and Consult Hyperion, KYC compliance costs banks €50 million a year. The potential cost of losing just a small percentage of potential new customers to complex manual KYC processes is now as much as €10 million a year. After five years, the cumulative lost opportunity could cost banks in excess of €150 million.”

KYC compliance costs banks €50 million a year. The potential cost of losing just a small percentage of potential new customers to complex manual KYC processes is now as much as €10 million a year.

This is a key point that organizations must consider, as whilst investing in a robust KYC process might seem costly, the loss of potential business could be far more substantial. Furthermore, there is also the cost of financial penalties which might be received, which must also be considered.

Proactive Risk Management

Fraud risk management is a key reason why a customer might choose one financial institution over another. A recent study found that 69% of consumers now prioritize fraud protection when deciding between financial institutions, highlighting the importance of a secure customer identification program and ongoing monitoring for any risk factors.

There are many kinds of scams that take place on financial platforms, including the creation of new accounts using a false or stolen identity, account takeovers, unauthorized credit or loan applications, and more. Some of the critical protections needed to instill loyalty and trust among customers might include:

- Safeguarding accounts with biometric authentication makes account takeovers much more difficult to carry out.

- A secure identity verification process that leverages liveness detection technology to quickly and effectively identify synthetic identities, stolen identities, or false identities. This allows businesses to quickly stop fraudsters from applying for credit or loans and stop them from opening an account in someone else’s name.

- The use of ongoing monitoring with fraud alerts and notifications. Giving customers real-time alerts when potentially fraudulent activities are detected on their accounts is crucial to building customer trust.

In addition, strict AML screening, which might include sanctions and PEP screening, adverse media checks, watchlist screening, and continuous monitoring, ensures full AML compliance, fostering increased digital trust.

Advanced Fraud Detection

Fraud detection has come a long way with new AI-powered technologies. Powering KYC processes with market-leading AI tools helps build a trustworthy global reputation. Some of the latest technologies include:

Liveness Detection

Liveness detection can identify stolen or false identities. It uses AI to pull biometric data from a submitted video during customer onboarding to verify whether or not the individual is a real person. Leveraging liveness detection ensures that businesses spot deepfake technologies during these onboarding processes, analyzing subtle micro-expressions and skin texture to ensure liveness. The customer’s identity is verified effectively, meeting KYC regulations when used with an advanced document verification check. For more on liveness detection, read “Liveness Detection: Best Practices for Anti-Spoofing Security.”

Optical Character Recognition

Optical Character Recognition (OCR) helps extract data from images of KYC documents quickly and effectively, verifying a client’s identity. OCR technology extracts key data points (e.g., name, date of birth, address) from identity documents, ensuring no manual errors or inconsistencies occur.

This extracted information can then be cross-checked against databases, such as sanctions lists, politically exposed persons (PEP) lists, and watchlists, to identify high-risk individuals. OCR can identify anomalies within images of government-issued KYC documents, which might indicate fraudulent tampering. Find more information on OCR here.

KYC Requirements as a Competitive Advantage

In the past couple of years, sophisticated KYC compliance processes within financial institutions to prevent fraud have become a clear competitive advantage. Customers look for platforms that can protect them at all times, especially since so many financial institutions have recently been victims of large-scale scams.

45% of all adverse contributions in the finance sector in 2023 were linked to stolen identities and identity fraud.

The banking sector has emerged as a key target for identity theft and synthetic identity fraud. According to Synectics Solutions, which manages the UK’s largest syndicated risk intelligence database, 45% of all adverse contributions in the finance sector in 2023 were linked to stolen identities and identity fraud. Fraudsters leverage falsified or stolen identities to drain funds from accounts, make unauthorized purchases, or fraudulently secure loans.

Differentiating Through Compliance

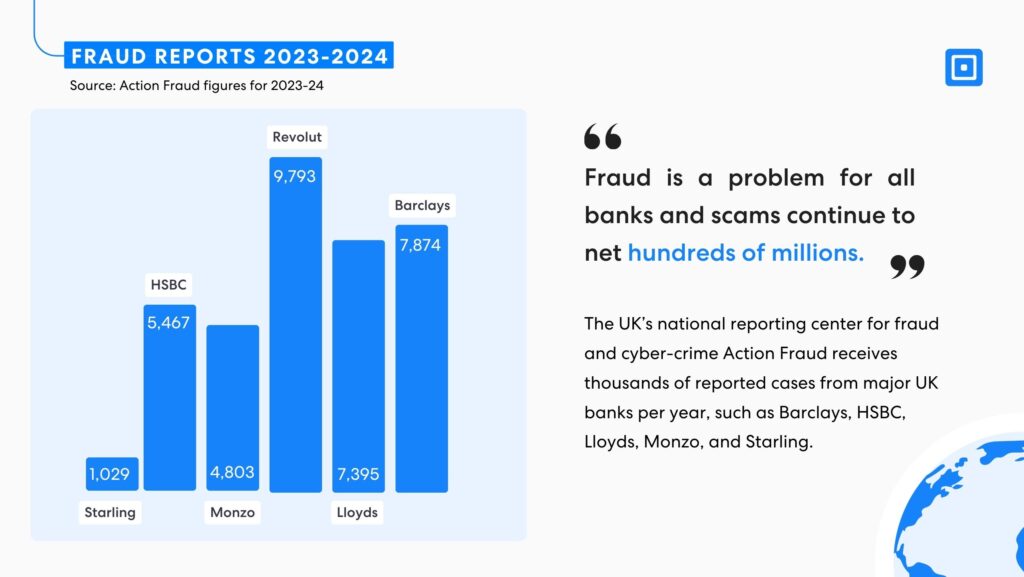

Between 2023 and 2024, fraud reports surged across major financial institutions, with HSBC receiving 5,467 reports, Revolut 9,793, Lloyds 7,395, and Barclays 7,874. These figures highlight the pervasive and sophisticated nature of modern fraudulent practices, underscoring the urgent need for financial institutions to reassess their priorities in order to win over customer trust and loyalty. For more information on identity fraud within UK financial institutions, read “Revolut Falls Victim to Identity Fraud.”

Stringent KYC processes will also enable businesses to operate in highly regulated markets, supporting global market expansion. This positions organisations as reliable international players, providing reassurance for investors and instilling confidence in customers and stakeholders.

Businesses that can differentiate themselves through reliable fraud defenses will continue to hold a competitive advantage within their industry as customers continue to prioritize security. An organisation that remains compliant with worldwide KYC and AML regulations, maintaining a strong reputation of security, is far more likely to win over a customer.

What Does a Comprehensive KYC Process Look Like?

For a KYC process to be a robust defense against fraud and ensure compliance, several key steps must be implemented. Some of these include:

Advanced Document Check: A document check will verify a government-issued identity document, checking for signs of tampering and extracting key information with OCR technology.

Biometric Verification with Liveness Detection: Biometric verification will quickly identify presentation attacks, such as those using deepfake technology. Biometric data samples are pulled from submitted images and videos to be examined, and details such as skin texture and subtle involuntary movements are analyzed.

Multi-Bureau Checks: With a Multi-Bureau Check, businesses can verify customer details, such as name, address, date of birth, and social security numbers, against trusted, authoritative sources such as government and credit bureaus.

Compliance with ComplyCube

ComplyCube offers state-of-the-art KYC solutions to help businesses safeguard their customers and their platforms from fraud. Achieving compliance across complex regulatory structures enables businesses to scale quickly and seamlessly, which ComplyCube’s platform supports.

For more information on fortifying your business with a robust KYC process, get in touch with one of our compliance experts.