Businesses need to strike the perfect balance between speed and security when implementing a comprehensive identity verification service. Digital identity verification plays a crucial role in fraud prevention by helping to verify users’ identities and ensuring that bad actors are prevented from accessing services or completing transactions. With the rise of digital services, the onboarding process must be efficient yet thorough, meeting regulatory requirements while maintaining security.

Automated processes can streamline customer onboarding, allowing organizations to quickly verify a person’s identity with documents like government-issued ID, proof of address, and even biometric data such as a phone number or camera image. A verification service integrated with an organization’s website or web portal can enable quick and reliable business verification, which is crucial to protect both customers and businesses from fraud. These systems can address risks, such as adverse media or incorrect data records, that may arise during verification.

By leveraging technology, businesses can handle the demands of multiple markets and industries, ensuring compliance while serving more users and meeting customer expectations. With these integrations, businesses can ensure a smooth onboarding experience, offering users easy access to their accounts and ensuring the transactions they complete are secure. The ability to prove a customer’s identity online is essential to prevent fraud, comply with regulations, and protect against the risks associated with fake information while providing customers with the speed they need in today’s fast-paced world.

The Hidden Bottleneck: KYC and the Slow Identity Verification Process

At its core, KYC is designed to ensure that financial institutions know exactly who their customers are. The process typically involves verifying government-issued IDs, proof of address, and, in some cases, additional documents, such as bank statements or utility bills. While these safeguards are essential for regulatory compliance, they often lead to significant delays when done manually, which is where startups face a major issue.

Many financial services companies still rely on outdated or inefficient manual processes, which makes the KYC verification stage a bottleneck. This delays customers’ access to services, creating friction in the onboarding process and frustrating users who expect faster, more seamless interactions.

For startups that aim to scale, these delays can be especially damaging:

- Increased Drop-Off Rates: Long verification times cause potential customers to abandon the onboarding process, which leads to lost business.

- Manual Effort Strain: Relying on manual checks for each customer means that a growing customer base demands more administrative time, resources, and costs, reducing the startup’s agility.

- Compliance Risk: With constantly evolving regulations, manual verification increases the risk of errors, compliance missteps, and regulatory penalties.

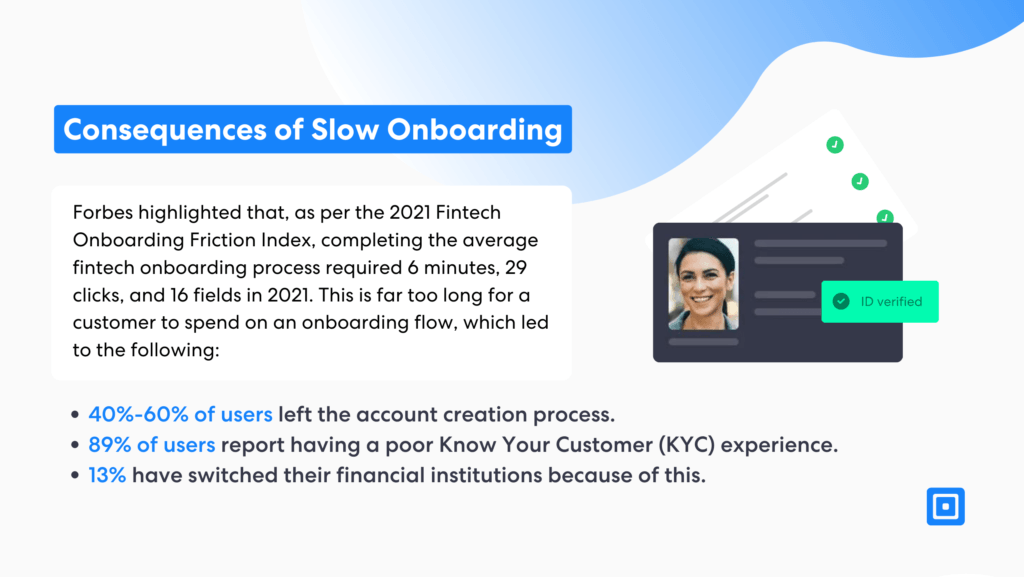

Forbes highlighted that, as per the 2021 Fintech Onboarding Friction Index, completing the average fintech onboarding process required 6 minutes, 29 clicks, and 16 fields in 2021. This is far too long for a customer to spend on an onboarding flow, which led to the following:

- 40%-60% of users left the account creation process.

- 89% of users report having a poor Know Your Customer (KYC) experience.

- 13% have switched their financial institutions because of this.

Onboarding remains a significant area of friction and cost for companies. Yet, the task of understanding your customer doesn’t stop after the initial setup. Personal details such as addresses and financial information are subject to change over time.

Partnering with an expert KYC platform can reduce onboarding time to less than 30 seconds per customer, granting businesses the ability to onboard customers seamlessly and scale. For this reason, partnering with a KYC platform with advanced technology is critical for growth and efficiency.

Evolving KYC Regulations: A Constant Challenge

KYC regulations are not static. They vary greatly across regions, and, in some cases, these rules are changing rapidly to meet the growing threats of digital fraud, money laundering, and terrorism financing. While these regulations are designed to enhance security, they can also contribute to significant delays if not addressed with the proper tools.

- Country-Specific Compliance: Financial institutions must tailor their KYC practices to comply with local laws. This means that startups planning to scale internationally face a complex web of compliance challenges. For example, U.S. regulations might require multiple forms of ID, while European Union regulations might demand proof of source of funds for certain transactions. Staying on top of these country-specific regulations is a daunting task and could cause further delays if handled manually.

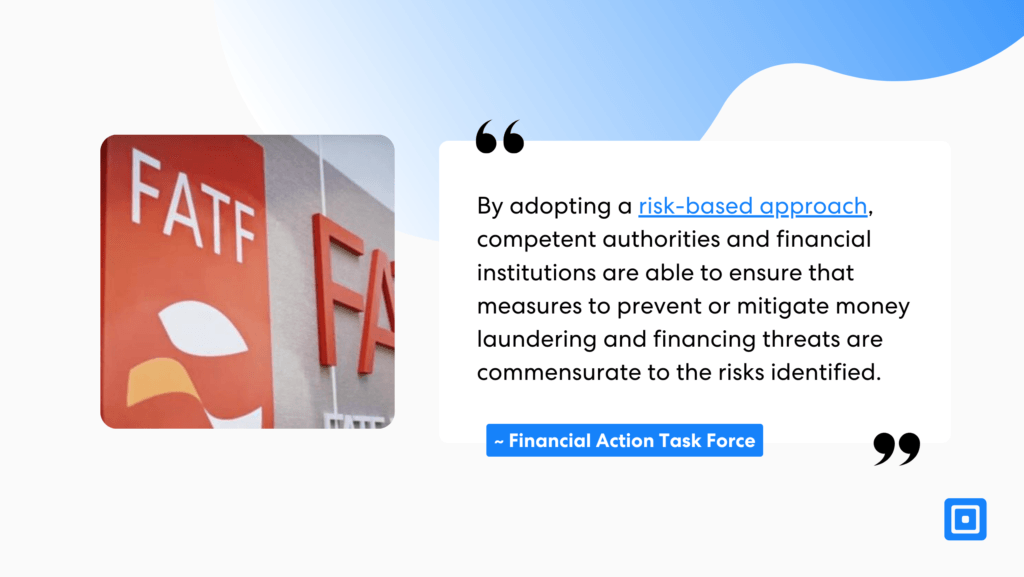

By adopting a risk-based approach, competent authorities and financial institutions are able to ensure that measures to prevent or mitigate money laundering and financing threats are commensurate to the risks identified. ~ FATF

- The Need for a Risk-Based Approach: Some regulators are shifting to a more dynamic, risk-based approach to KYC, meaning that higher-risk customers, such as those from certain countries or industries, will require more intensive verification. However, identifying these customers and adjusting the verification process is time-consuming when done manually. For startups with limited resources, this complexity becomes a scalability challenge. Automation tools that can differentiate risk levels and apply different levels of scrutiny are essential to ensure efficiency and compliance.

Staying ahead of regulatory changes and emerging risks manually is time-consuming and costly for businesses of all sizes. Along with identity checks, a highly time-consuming part of manual AML checks is screening each client separately against multiple lists, including PEP databases and sanctions lists. For companies managing large client bases, this involves reviewing every individual’s profile, comparing it to both national and international databases, and frequently performing further investigations into negative media coverage or the origins of their wealth.

Remote KYC: The Digital Shift for a Faster, More Efficient Process

The rise of remote services has placed additional pressure on startups to streamline their KYC processes. Customers now expect to complete identity verification without leaving their homes, and a slow, in-person verification process just won’t cut it in today’s digital-first environment. This is where remote identity verification solutions can play a crucial role in eliminating bottlenecks.

Document Verification through AI: AI-powered tools can scan, validate, and cross-check government-issued IDs and documents within seconds. These tools use machine learning algorithms to detect fraudulent documents or suspicious activity, making them far more efficient and accurate than manual review. For startups, this enables them to serve more customers without hiring an army of compliance staff.

Facial Recognition and AI Integration: Biometric identity verification is fast becoming the gold standard for digital KYC. Through facial recognition and liveness detection technology, users can verify their identity in real-time, reducing the need for physical document submission or face-to-face meetings. This shift not only accelerates the onboarding process but also minimizes human error and enhances security.

How Digital Identity Solutions Can Drive Startup Growth

The move to digital identity verification is essential for startups looking to scale without hitting identity verification bottlenecks.

- Instant Onboarding: By incorporating AI-powered solutions like selfie-based verification or digital ID verification, customers can complete the entire KYC process in minutes instead of days. This seamless experience helps startups create a frictionless path to onboarding, encouraging more customers to join and reducing abandonment rates.

- Improved Customer Satisfaction: The quicker and more secure the verification process, the better the overall user experience. With instant identity validation, customers no longer have to wait for days to complete the KYC process or submit additional paperwork. This creates a positive first impression and builds customer trust immediately.

- Cost Efficiency and Scalability: For startups, the key to scaling is automation. As your customer base grows, manual verification becomes unsustainable. Automated KYC platforms can easily handle large volumes of verifications without compromising speed or accuracy. This allows startups to focus their resources on scaling other business areas while ensuring regulatory compliance and customer satisfaction.

Embracing the Future of KYC for Scalable Growth

For startups in the financial services sector, slow and manual identity verification processes are holding them back. KYC compliance is necessary, but outdated practices create a bottleneck that leads to frustrated customers, high drop-off rates, and hindered scalability.

The future of KYC is in automation, remote verification, and AI-powered solutions. By embracing these technologies, startups can streamline their verification processes, meet compliance regulations, and provide a seamless, secure, and fast onboarding experience. This allows them to scale effectively, remain competitive, and serve a growing customer base without sacrificing security.

Contact one of our compliance experts for more information on how to implement advanced IDV and KYC solutions to safeguard your organization.